What Most Veterans Don’t Know About Their VA Home Loan Benefit

You served. You earned this benefit. And there is a real chance it could get you into a home sooner than you think, even in today’s market.

According to a recent survey from NewDay USA, nearly half of Veterans, 49%, feel that homeownership is currently out of reach. But the data tells a different story. Most of those Veterans are closer than they realize. The problem is not eligibility. The problem is misinformation. Three specific misconceptions keep Veterans from using a benefit they have already earned, and clearing them up could change everything about your timeline.

Misconception One: You Need a Large Down Payment

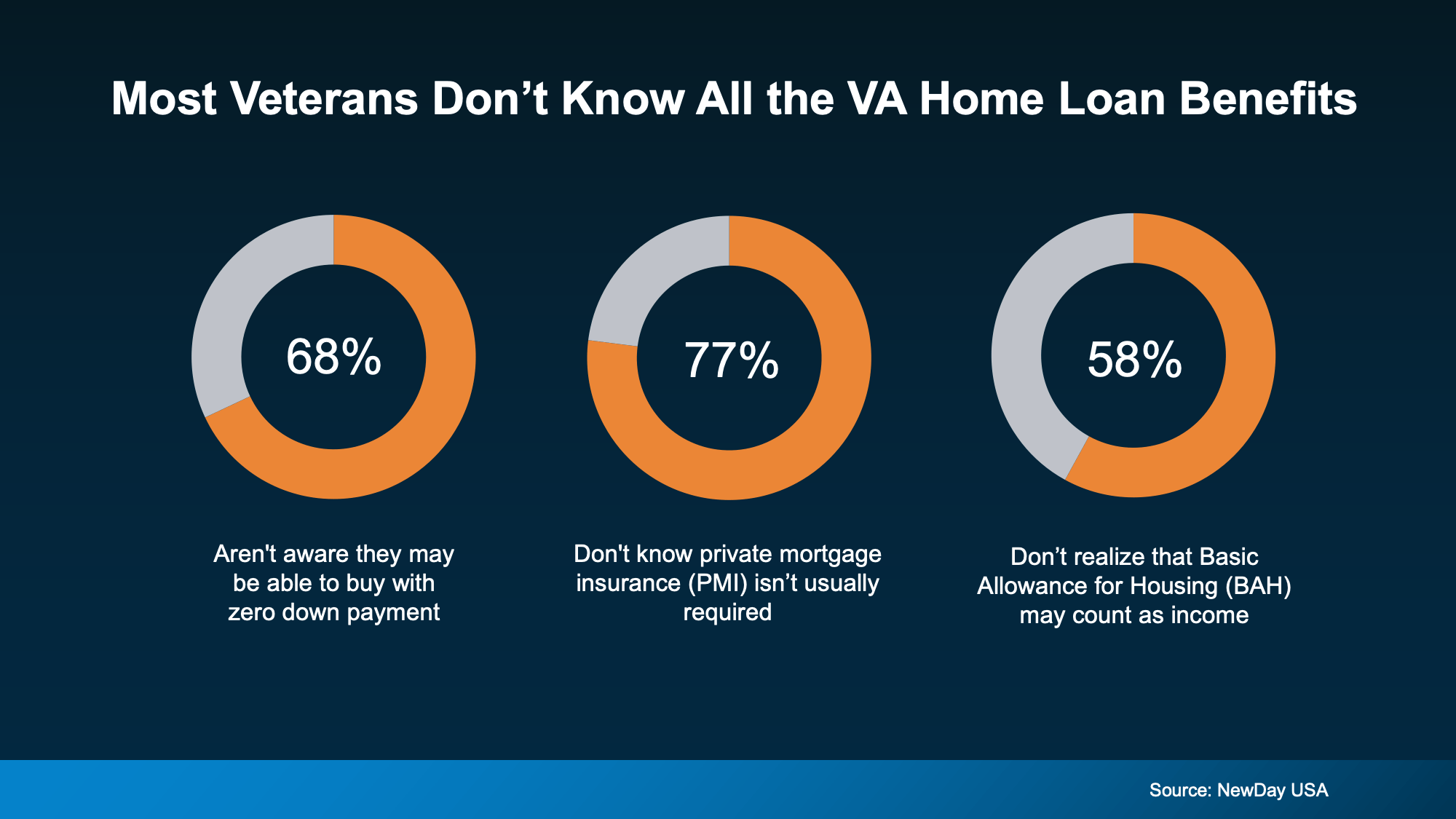

This is the biggest one, and it stops more Veterans than anything else. The NewDay USA survey found that many Veterans assumed they needed to save somewhere between $10,000 and $19,900 before they could buy. That assumption alone can push homeownership years into the future.

Here is the reality. VA loans can require zero down payment for eligible borrowers. Not a small down payment. Zero. That is not a promotional offer or a special program you have to hunt for. It is a core feature of the VA home loan benefit that has been in place for over 80 years. If you have been putting off buying because you have not saved enough for a down payment, it is worth finding out whether the VA benefit removes that barrier entirely. And if you are wondering whether any other options exist to help with upfront costs, Getting a Tax Refund? Here’s How It Can Help You Buy a Home is worth a read alongside this one.

Misconception Two: Closing Costs Will Still Be Expensive

Even buyers who know about the zero down payment option often assume closing costs will eat up whatever savings they have. That is not necessarily true either. According to the Department of Veterans Affairs, VA loans come with limits on the types of closing costs buyers are required to pay. That means more money stays in your pocket on closing day and less cash is needed upfront before you can move in. Combined with the down payment advantage, this can dramatically shorten the time it takes to get from “thinking about buying” to “keys in hand.”

Misconception Three: You Still Have To Pay Private Mortgage Insurance

Private mortgage insurance, or PMI, is one of the more frustrating costs of conventional financing. If you put down less than 20% on a conventional loan, you typically pay PMI every single month until you reach 20% equity. According to NewDay USA, that can run anywhere from $100 to $300 per month depending on your loan size. Over five years, that is potentially $18,000 in additional costs that build zero equity.

VA loans do not require PMI, even with no money down. That monthly savings compounds quickly and makes the overall cost of homeownership through a VA loan significantly lower than most Veterans realize when they are running their initial numbers. For a full breakdown of how affordability stacks up right now across all loan types, see The Truth About Home Affordability Today.

One More Thing: Your BAH and BAS May Count Toward Income Qualification

If you are active duty or a qualifying reservist, your Basic Allowance for Housing and Basic Allowance for Subsistence may count as qualifying income on a VA loan application. Both are non-taxable, which can actually improve your qualifying position. If you ran the affordability numbers without factoring these in, you may qualify for more than you thought. It is also worth understanding how the broader rate environment affects what you qualify for, which we break down in What Rising Inflation Means for Your Move.

Rates Are Still Workable, Especially With the VA Advantage

A question we hear often from Veterans is whether today’s rates make the VA benefit less valuable than it used to be. The answer is no, and in some ways the opposite is true. When rates are elevated, every advantage that lowers your monthly payment or reduces your upfront costs matters more, not less. The elimination of PMI alone is worth hundreds of dollars a month in a higher rate environment. For context on where rates are headed and what that means for buyers planning their timing, our Mid-Year Housing Market Reality Check lays out the full picture.

What This Means for Veterans Buying in South Jersey

South Jersey and the Philadelphia suburbs have a strong mix of single-family homes, townhomes, and condos at price points where the VA benefit can make a real and immediate difference. No down payment requirement combined with no PMI and reduced closing costs is a genuinely powerful combination in a market where affordability is the primary challenge for most buyers right now.

If you are a first-time buyer using your VA benefit for the first time, our Step-by-Step Guide to Buying Your First Home in NJ walks through the full process so you know exactly what to expect. And if budget is a consideration, Less House, More Home: Why Smaller Homes Are Paying Off for Today’s Buyers explores how buyers are finding real value in today’s market even with tighter numbers.

The benefit exists. You earned it. The only question is whether you are using it.

Reach out to the MH Global team. We work with Veterans regularly and can connect you with a VA-experienced lender who will walk you through exactly what you qualify for. You may be able to buy a home sooner than you thought.