What Rising Inflation Means for Your Move

Inflation is moving in the wrong direction. You’ve probably felt it at the gas pump, the grocery store, and just about everywhere else. And if you’ve got a move on your mind, you’re right to wonder what it means for the housing market.

Here’s the full picture, grounded in the actual data, so you can make decisions based on facts rather than fear.

Inflation Is Up. Here Is What That Actually Means.

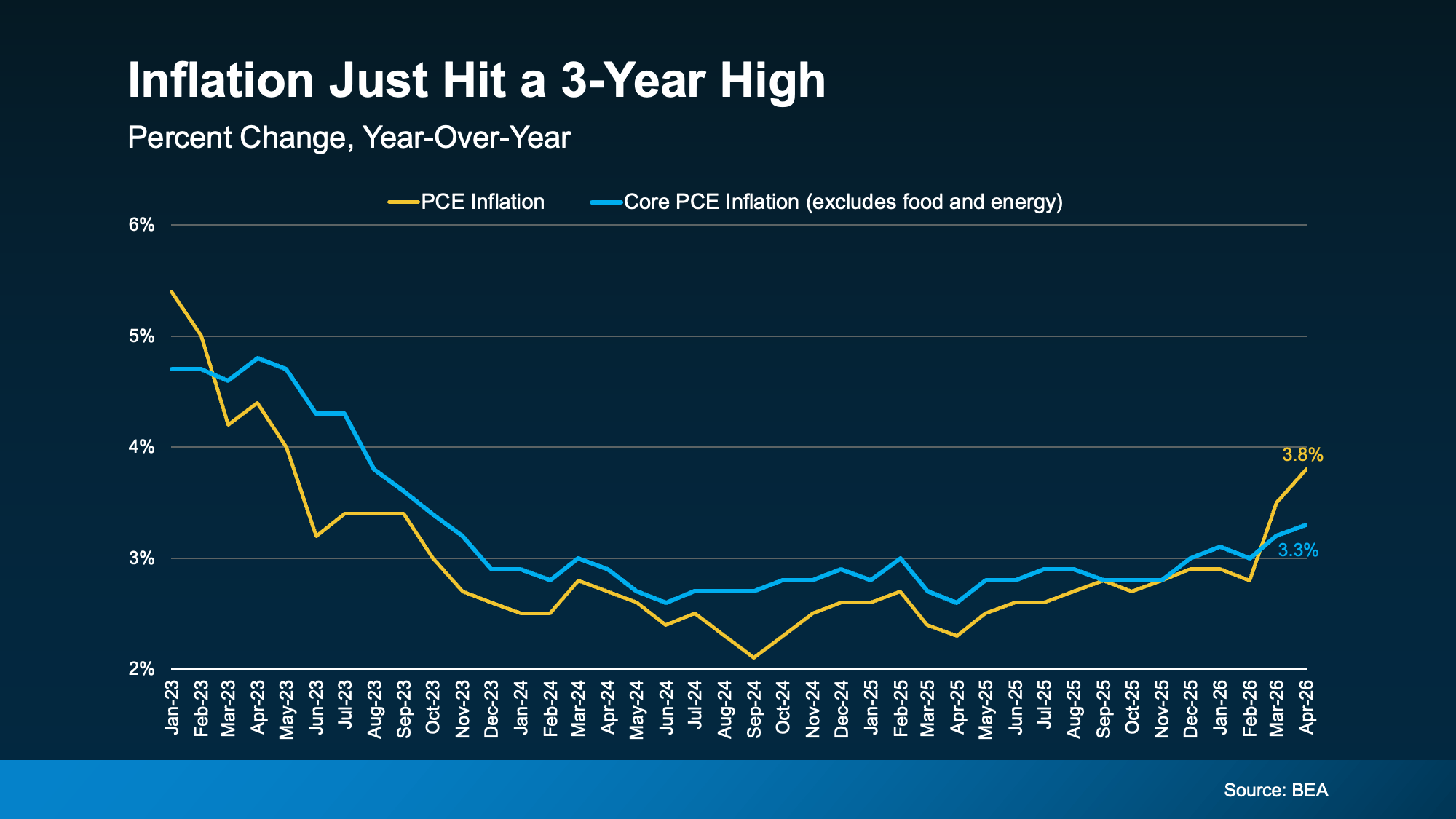

The government tracks inflation in several ways. One of the most closely watched is the PCE, or Personal Consumption Expenditures Price Index, published by the Bureau of Economic Analysis. It measures how much more, or less, people are paying for goods and services compared to a year ago. Based on your own expenses lately, you can probably guess which direction it’s heading.

Overall PCE has spiked sharply since February, driven in large part by the ongoing conflict in the Middle East pushing gas and energy prices significantly higher.

But here is the somewhat encouraging part. There is a second measure called core PCE, which strips out gas and energy prices because they swing around so much they can distort the picture. The Federal Reserve actually watches core PCE most closely when making interest rate decisions. And while core PCE is rising, it is not rising nearly as fast as the headline number. That tells us a meaningful portion of this inflation spike is tied directly to what is happening overseas. When that situation stabilizes, inflation may ease along with it.

Why This Matters Directly for Mortgage Rates

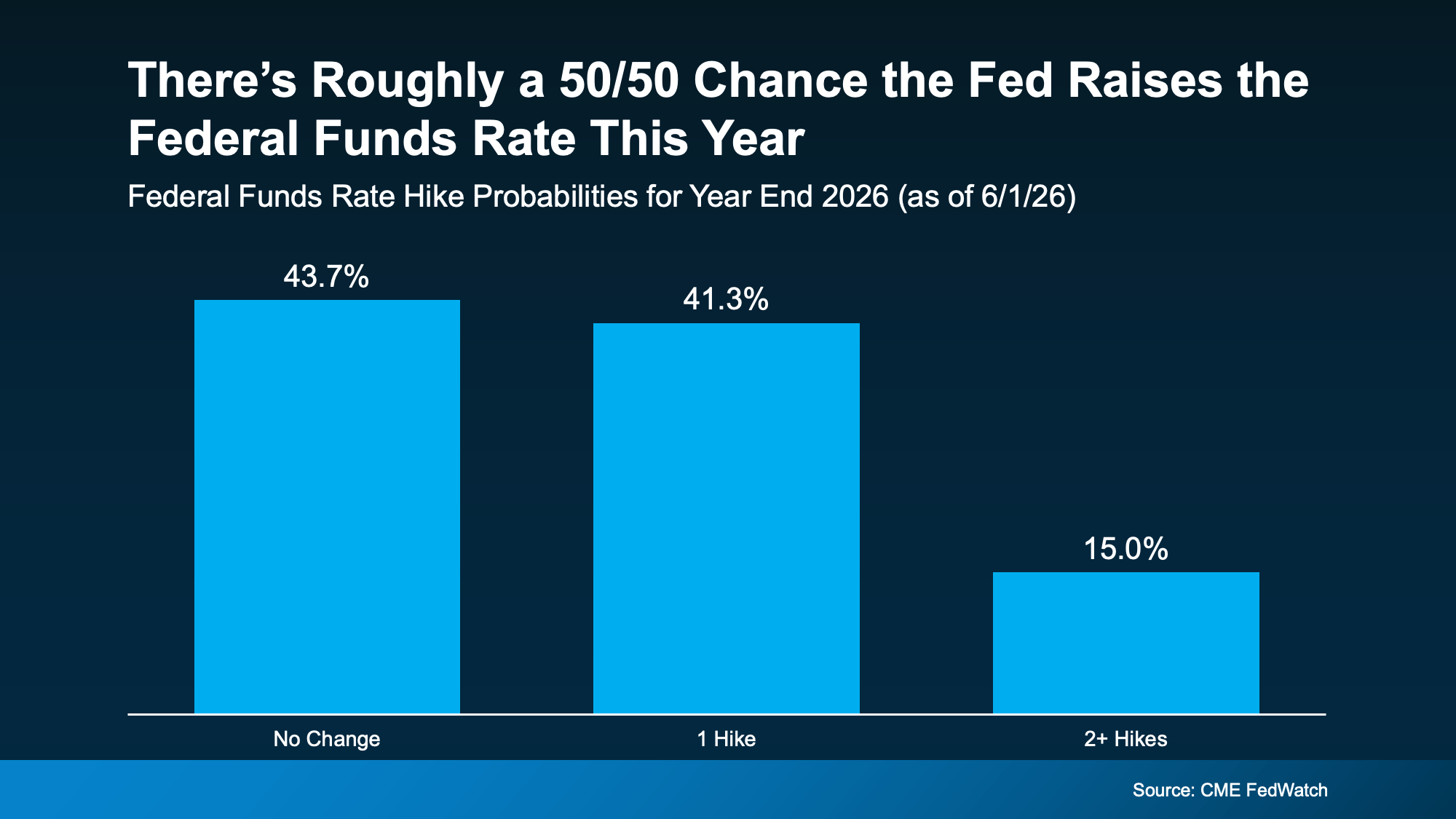

Here is the housing connection. When inflation runs high, the Fed tends to keep the Federal Funds Rate elevated, or even raise it, to slow spending and cool prices back down. That rate does not move mortgage rates in a one-for-one way, but it absolutely has an influence on what you pay when you borrow.

Right now, CME FedWatch is showing roughly a 50/50 chance the Fed raises the Federal Funds Rate before the end of 2026. That is not a certainty, but it is a real possibility, and it matters for anyone hoping rates will drop soon.

As Bankrate put it plainly: oil prices and bond yields have come down slightly but are still well above where they were at the start of spring. Until there is a resolution to the conflict overseas, both inflation and mortgage rates are likely to stay elevated.

If you have been waiting for a significant rate drop before making your move, this data is a clear signal that “higher for longer” is still very much on the table.

But This Is Not 2008. Not Even Close.

A tough economy is not the same thing as a housing crash. It is worth saying that directly, because the headlines have a way of blurring that distinction. The conditions that caused the 2008 collapse are simply not present today. Here is why:

Inventory is still relatively low. There is no flood of distressed homes hitting the market. We covered why foreclosure fears are overblown in detail in What the Foreclosure Headlines Aren’t Telling You. Most homeowners today are sitting on significant equity, which we break down in Record High Mortgage Debt Sounds Scary. Here’s What the Headlines Leave Out. Lending standards are also far stricter than they were before 2008, which means the wave of underwater borrowers that triggered the last crash is not building beneath the surface today.

Uncomfortable and unhealthy are not the same thing. The market is hard right now. Hard and crashing are very different situations.

You Still Have Options. Here Is What To Do.

High rates do not put homeownership out of reach. They just change the path you take to get there. A few strategies worth discussing with your lender and agent:

Adjustable-rate mortgages can offer a lower rate upfront, which may make the monthly payment more manageable in the short term. We covered how ARMs work and who they make sense for in Thinking About an Adjustable-Rate Mortgage? Here’s What You Need To Know. Rate buydowns, where you pay points upfront to lower your rate, are another option worth asking about. First-time buyer programs and down payment assistance programs also exist specifically for markets like this one, and they are underutilized. And if you have a tax refund sitting in your account, Getting a Tax Refund? Here’s How It Can Help You Buy a Home walks through exactly how to put that toward your purchase.

The right strategy tailored to your situation will always matter more than waiting for a perfect moment that may not come on your timeline.

What This Means for Buyers and Sellers in South Jersey Right Now

Inflation and rate volatility affect every market, but they do not affect every market equally. South Jersey and the Philadelphia suburbs have specific inventory levels, price dynamics, and buyer activity that shape what is actually possible for you right now. Our South Jersey Real Estate Market Update 2026 gives you the local context that national inflation headlines cannot.

The bottom line is this: inflation is real, rates are elevated, and the path forward requires more strategy than it did a few years ago. But the path is there. And the buyers who are working with the right team right now are finding it.

Reach out to the MH Global team. Let’s build a plan that works for your situation today.