What the Foreclosure Headlines Aren’t Telling You

When you see a headline saying foreclosures are rising, it is natural for your mind to jump to 2008. That crash left a mark on an entire generation of homeowners and buyers, and nobody wants to see it happen again. But here is what those headlines are leaving out: context. And without context, a rising number looks alarming even when the reality is far more stable than the story being told.

Foreclosures Are Rising. But Rising From Where?

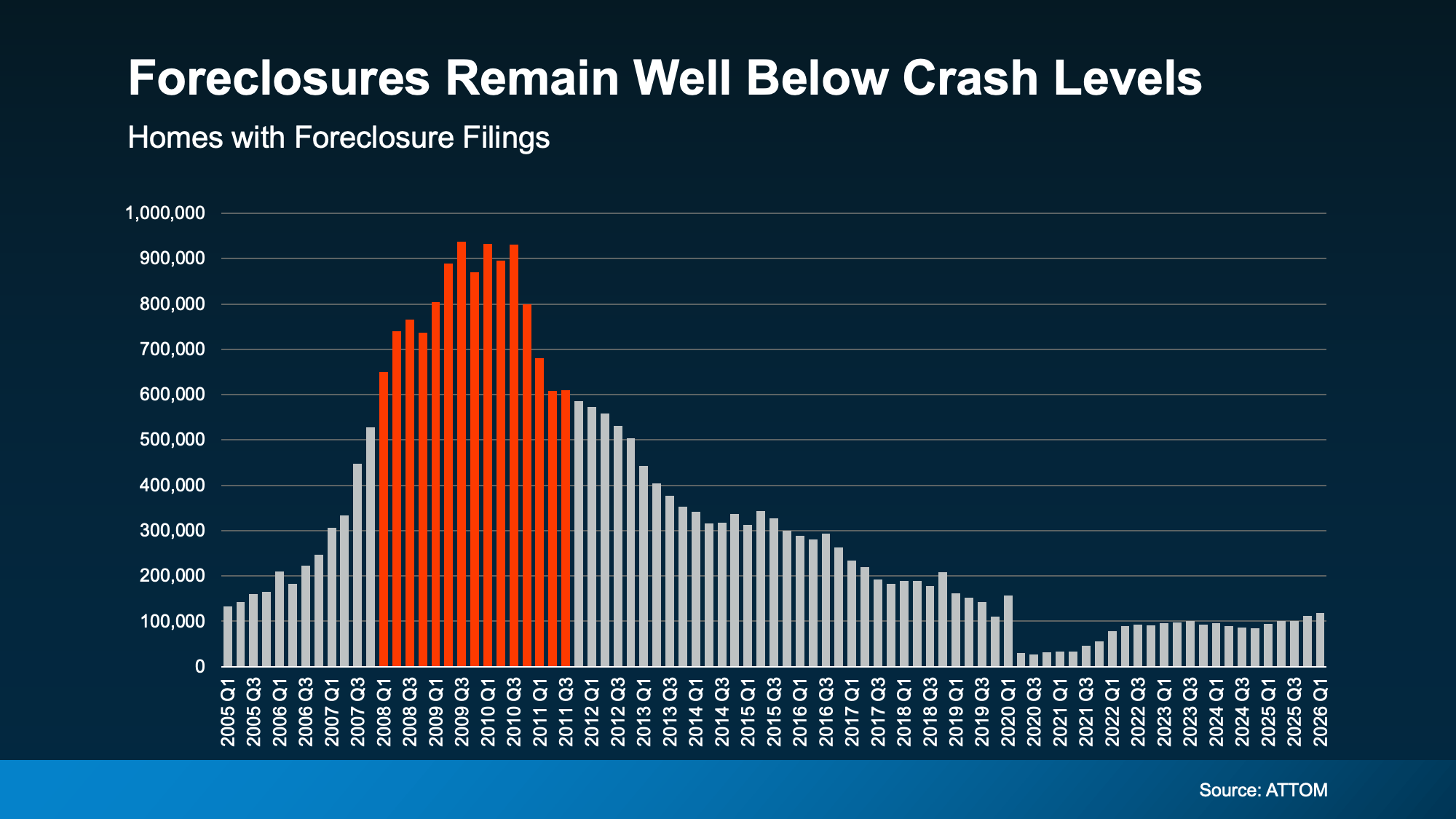

Yes, foreclosure filings are up 26% year over year according to the ATTOM Q1 and March 2026 Foreclosure Market Report. And they have been rising for five straight quarters. That is a real trend and worth paying attention to. But the critical question is not whether foreclosures are up. It is what they are up compared to.

The baseline everyone is measuring from is 2020 and 2021, when the government put a moratorium on foreclosures to protect homeowners during the pandemic. Those numbers were artificially suppressed to historic lows that do not represent anything close to normal market activity. Comparing today to that period is like comparing a drought year to a flood year and concluding we must be underwater.

The more meaningful comparison is to 2017, 2018, and 2019, the last years the housing market operated normally before the pandemic distorted everything. By that measure, today’s foreclosure numbers are still below pre-pandemic norms. We are not even back to what is typical yet, which means this is a normalization, not a crisis.

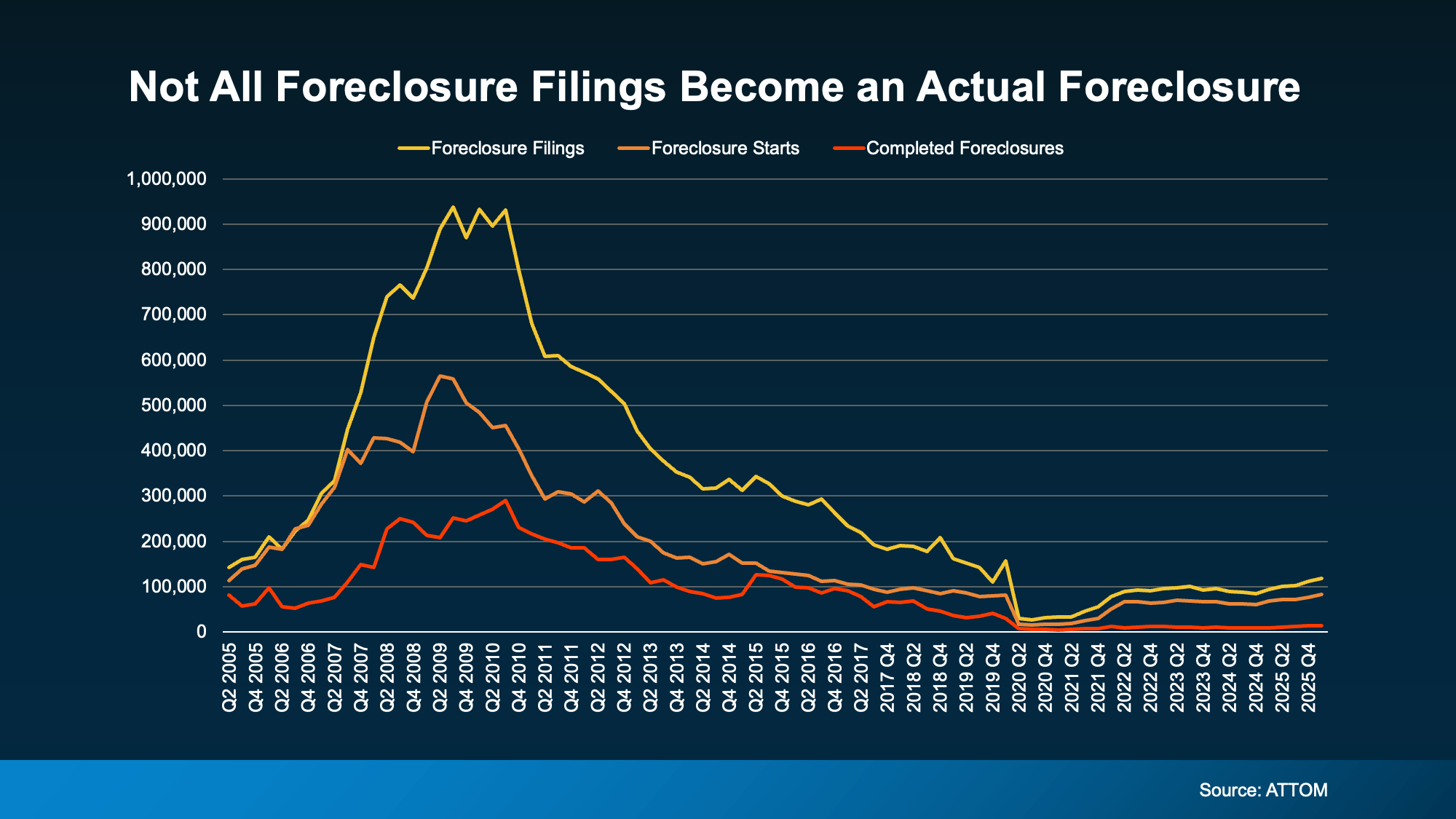

Most Foreclosure Filings Never Become Completed Foreclosures

This is the detail that almost never makes it into the headline. The ATTOM data tracks three distinct categories: total foreclosure filings, foreclosure starts where the process has officially begun, and completed foreclosures where a homeowner actually loses their home. The completed foreclosure number sits well below the other two, and the gap between them tells the real story.

The reason most filings do not end in completed foreclosures is equity. According to Cotality, the average homeowner today is sitting on approximately $295,000 in home equity. When a homeowner gets into financial difficulty and has that much equity, they have a way out that 2008 homeowners simply did not have. They can sell, cover what they owe, protect their credit, and in many cases walk away with money remaining. That option eliminates the need for foreclosure in the majority of cases where the process begins.

Equity Is the Structural Difference Between Now and 2008

In 2008, the crisis was not caused by high foreclosure filings alone. It was caused by homeowners who owed more than their homes were worth, had no equity cushion, no ability to sell at a profit, and no option except to walk away. That dynamic created a flood of distressed inventory that crashed prices across entire markets.

Today, that condition does not exist. Home values have held steady and in most markets continued to rise, as we covered in Are Home Prices Going To Fall? Homeowners are not underwater. They have equity. And equity changes everything about how financial distress resolves in a housing market. For the broader picture of what the current debt and equity landscape looks like nationally, our post Record High Mortgage Debt Sounds Scary. Here’s What the Headlines Leave Out addresses this directly.

Lending Standards Prevent the Cascade That Caused 2008

Before the last crash, loose lending standards put people into homes they could not afford once rates adjusted or circumstances changed. Today, those standards are significantly stricter. Borrowers are evaluated on their genuine ability to repay, income is verified, and the loan pool is far healthier as a result. Even the adjustable-rate mortgages gaining popularity today are structured and underwritten very differently from the ones that defaulted en masse before. We break that down in Thinking About an Adjustable-Rate Mortgage? Here’s What You Need To Know.

If You Are Struggling, You Have More Options Than You Know

If you are behind on payments or worried about what comes next, it is important to know that missing one or two payments does not automatically mean you will lose your home. Lenders would much rather work with you than foreclose. The process is expensive and time-consuming for them too. Repayment plans, forbearance, and loan modifications are all tools lenders use to avoid foreclosure, and the sooner you reach out to your lender, the more options remain on the table.

It is also worth knowing that in New Jersey, foreclosure is a judicial process, meaning it must go through the court system. That process takes considerably longer than in non-judicial states, giving New Jersey homeowners more time to explore alternatives before losing a home. The key is acting early. The sooner you engage your lender, the more room there is to find a solution.

If selling makes more financial sense for your situation, that is worth exploring too, especially given how much equity most homeowners are currently holding. Our South Jersey Real Estate Market Update 2026 gives you a sense of what homes are actually selling for in our area right now.

What This Means for Buyers Watching From the Sidelines

If you have been waiting for a flood of distressed inventory to bring prices down, the data says that scenario is unlikely. The equity picture, lending standards, and current foreclosure completion rates all point toward a market that is normalizing, not destabilizing. For buyers who have been on the fence, our post Wondering If You Should Still Buy a Home Right Now?addresses exactly that question with current data. And 3 Things That Are Not Going To Happen in Today’s Housing Market clears up the other major misconceptions that are keeping buyers on the sidelines right now.

The market is not heading toward a crash. It is returning to normal. And normal is actually a good environment for buyers and sellers who approach it with the right strategy.

What This Means for Homeowners and Buyers in South Jersey

New Jersey’s judicial foreclosure process provides homeowners meaningful time and legal protection that does not exist in many other states. And South Jersey’s current market, with home values holding steady and demand remaining active across Camden, Burlington, and Gloucester counties, means that homeowners in financial difficulty who do need to sell are generally in a position to do so without catastrophic loss.

For buyers, the absence of a distressed inventory wave means prices are not heading downward. The opportunity in this market is not about waiting for a crash. It is about positioning yourself to move when the right home comes available.

Reach out to the MH Global team. Whether you are buying, selling, or trying to make sense of what the headlines actually mean for your situation, we will give you a straight answer based on real local data.