Thinking About an Adjustable-Rate Mortgage? Here Is What You Need To Know.

Adjustable-rate mortgages are getting more attention than they have in years. If you have been shopping for a home in today’s rate environment, you have probably heard the term. And if you grew up watching the 2008 housing crisis unfold, you may have an instinctive reaction to walk the other way. That reaction is understandable, but the full picture is worth understanding before you dismiss the option entirely.

ARMs Are Getting Popular Again. Here Is Why.

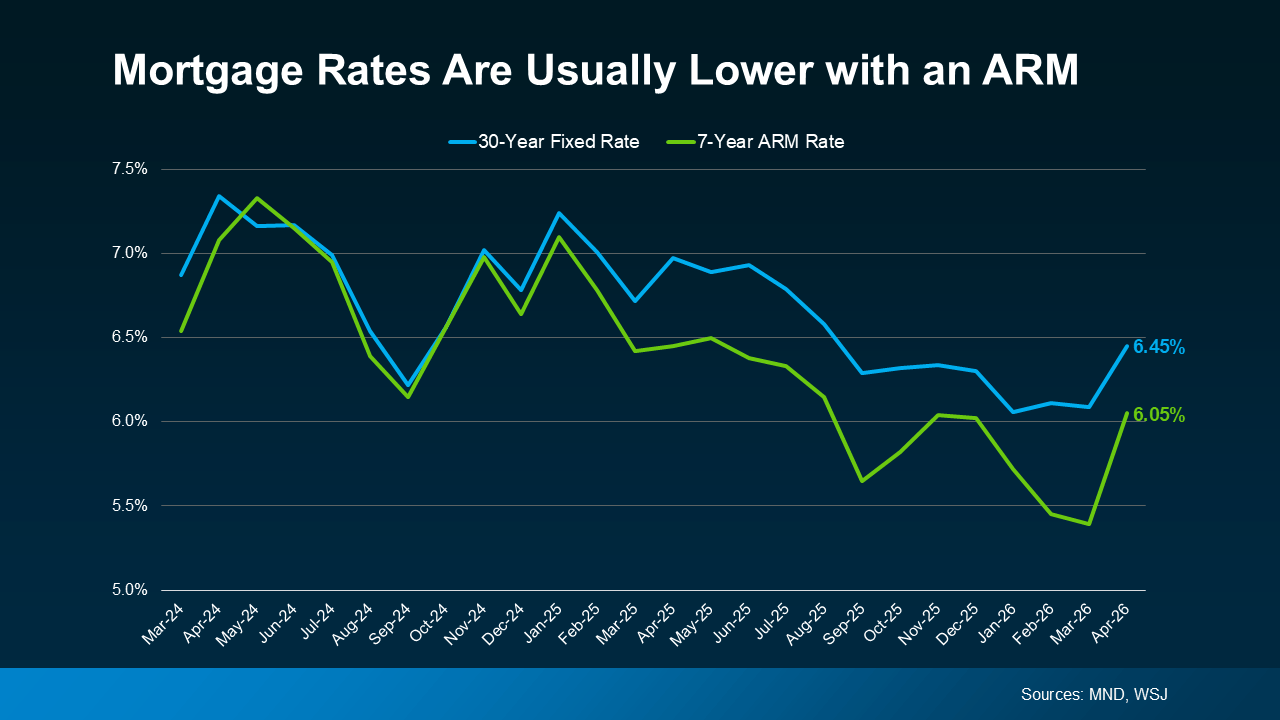

The reason is straightforward: affordability. Fixed rates have been sitting in the mid-to-upper 6% range, and for buyers trying to make the monthly payment work, the lower initial rate on an ARM can make a meaningful difference. According to research from Redfin, the typical buyer can save approximately $150 per month by choosing an ARM over a 30-year fixed mortgage at current rate spreads. For some buyers, that is the difference between qualifying and not qualifying. For others, it is simply better cash flow each month that makes owning feel sustainable rather than stretched.

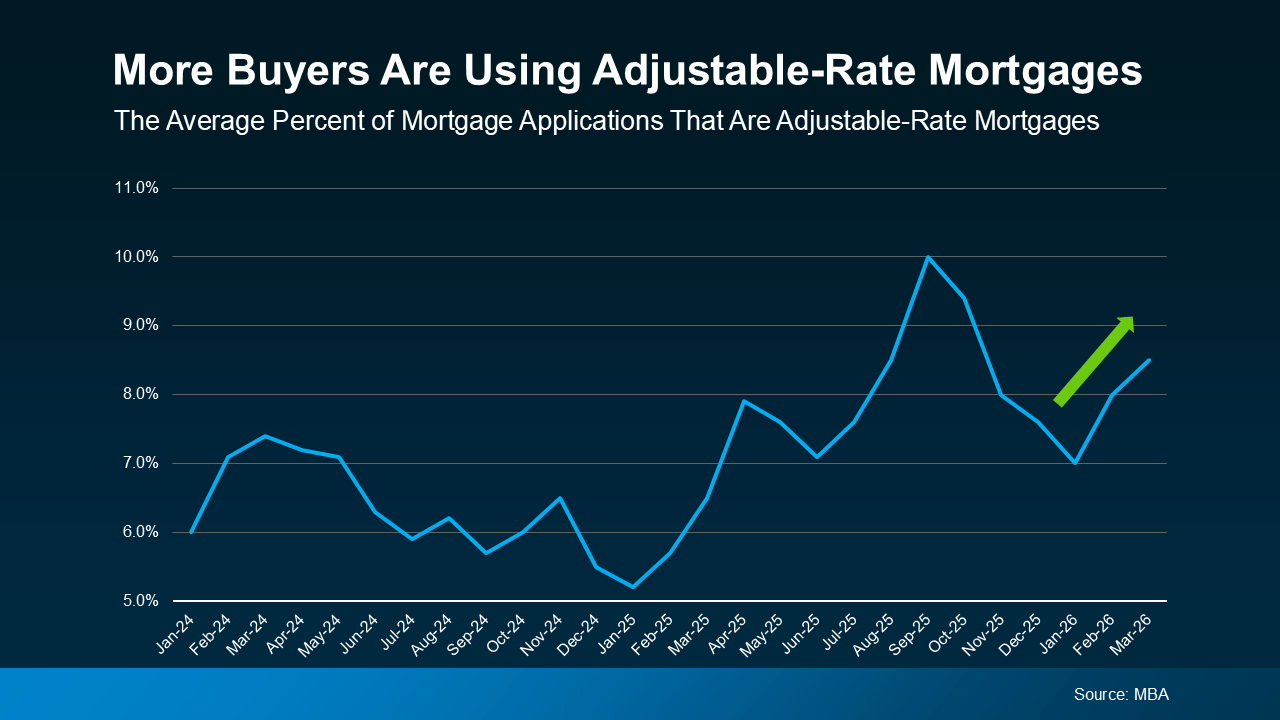

Data from the Mortgage Bankers Association shows the share of buyers choosing ARMs has been rising steadily, which reflects how many buyers are finding this a practical tool for navigating today’s market rather than waiting for fixed rates to drop.

How an ARM Actually Works

An adjustable-rate mortgage starts with a fixed rate for an initial period, typically 5, 7, or 10 years, and then adjusts periodically after that based on a market index. The most common structure today is a 5/1 ARM, which gives you five years at a fixed rate before it adjusts once per year. The initial rate is lower than a 30-year fixed, which is where the monthly savings comes from.

After the fixed period ends, your rate can go up or down depending on where the benchmark index sits at each adjustment date. There are caps that limit how much the rate can move at each adjustment and over the life of the loan, but it can increase meaningfully depending on market conditions.

According to Mortgage News Daily and the Wall Street Journal, the upfront rate on an ARM is currently lower than a 30-year fixed mortgage, which is exactly what is driving renewed buyer interest in this product.

Today’s ARMs Are Not the Same as the Ones That Caused Problems in 2008

This is the most important distinction to understand. Before the last housing crash, ARMs were frequently issued to borrowers who could not afford the payment once the rate adjusted, often with minimal income verification and teaser rates that were never sustainable. The collapse of those loans triggered mass defaults and foreclosures.

Today’s lending environment is fundamentally different. Lenders are required to evaluate whether borrowers can handle payment increases, not just the initial teaser rate. Income verification is strict. The loan structures themselves are more protective with built-in adjustment caps. Today’s ARMs reflect a mature, regulated product, not the loose instruments that fueled 2008. For more on why the current market bears no resemblance to 2008 conditions, our posts What the Foreclosure Headlines Aren’t Telling You and Record High Mortgage Debt Sounds Scary. Here’s What the Headlines Leave Out both address this directly.

When an ARM Makes Sense and When It Does Not

An ARM can be a smart choice in specific situations. If you know you are likely to move or refinance within the fixed period, you capture the lower rate with minimal exposure to the adjustment risk. If you expect your income to grow significantly over the next several years, the potential for a higher payment later may be manageable in a way it is not today. And if your primary goal is to buy now and refinance when fixed rates drop, an ARM gives you a lower payment in the interim.

An ARM is a riskier choice if you plan to stay in the home long-term and could not manage a higher payment if rates rise significantly after the fixed period ends. The right lender will walk you through specific scenarios showing what your payment would look like at various adjustment outcomes so you can make the decision with clear eyes. For broader context on how to evaluate your financing options in today’s market, our post Wondering If You Should Still Buy a Home Right Now? covers the full picture of what buyers are working with right now.

ARMs Are One Tool in a Broader Strategy

ARMs work best as part of a thoughtful financing plan, not as a standalone solution. Combining an ARM with the right purchase price, a builder rate buydown as covered in Newly Built Home Prices Hit a 5-Year Low, or strategic use of savings as outlined in Getting a Tax Refund? Here’s How It Can Help You Buy a Home can produce a monthly payment that works today while maintaining flexibility for what comes next.

For first-time buyers navigating all of these options for the first time, our Step-by-Step Guide to Buying Your First Home in NJ walks the full process from pre-approval through closing so nothing catches you off guard.

What This Means for Buyers in South Jersey Right Now

In a market where affordability remains the primary challenge, having every financing tool available and understanding how each one works is a genuine competitive advantage. Buyers who understand ARMs, buydowns, VA benefits, and down payment strategies are making moves while buyers who are waiting for perfect conditions are still renting.

Reach out to the MH Global team. We will connect you with a trusted lender who can run the real numbers on an ARM versus fixed for your specific situation so you can make the decision that is actually right for you.