Rent or Buy? The Real Tradeoff Most People Don’t Talk About

With home prices and mortgage rates where they are right now, renting can feel like the safe, sensible choice. And for some people in some situations, it genuinely is. But there is one part of this conversation that almost never gets the attention it deserves: what each choice does to your financial future over time. And that difference is larger than most people realize.

Renting Has Real Advantages, and Real Costs

Renting offers lower upfront costs, less maintenance responsibility, and more flexibility to move when your life changes. Those are legitimate benefits and worth weighing honestly. But a Bank of America survey found that 70% of aspiring homeowners worry about what long-term renting means for their future. That concern is grounded in something real.

When you rent, you pay for shelter. You do not build anything with those payments. No equity, no appreciation, no asset to leverage or pass on. Every dollar goes to your landlord’s mortgage, not yours.

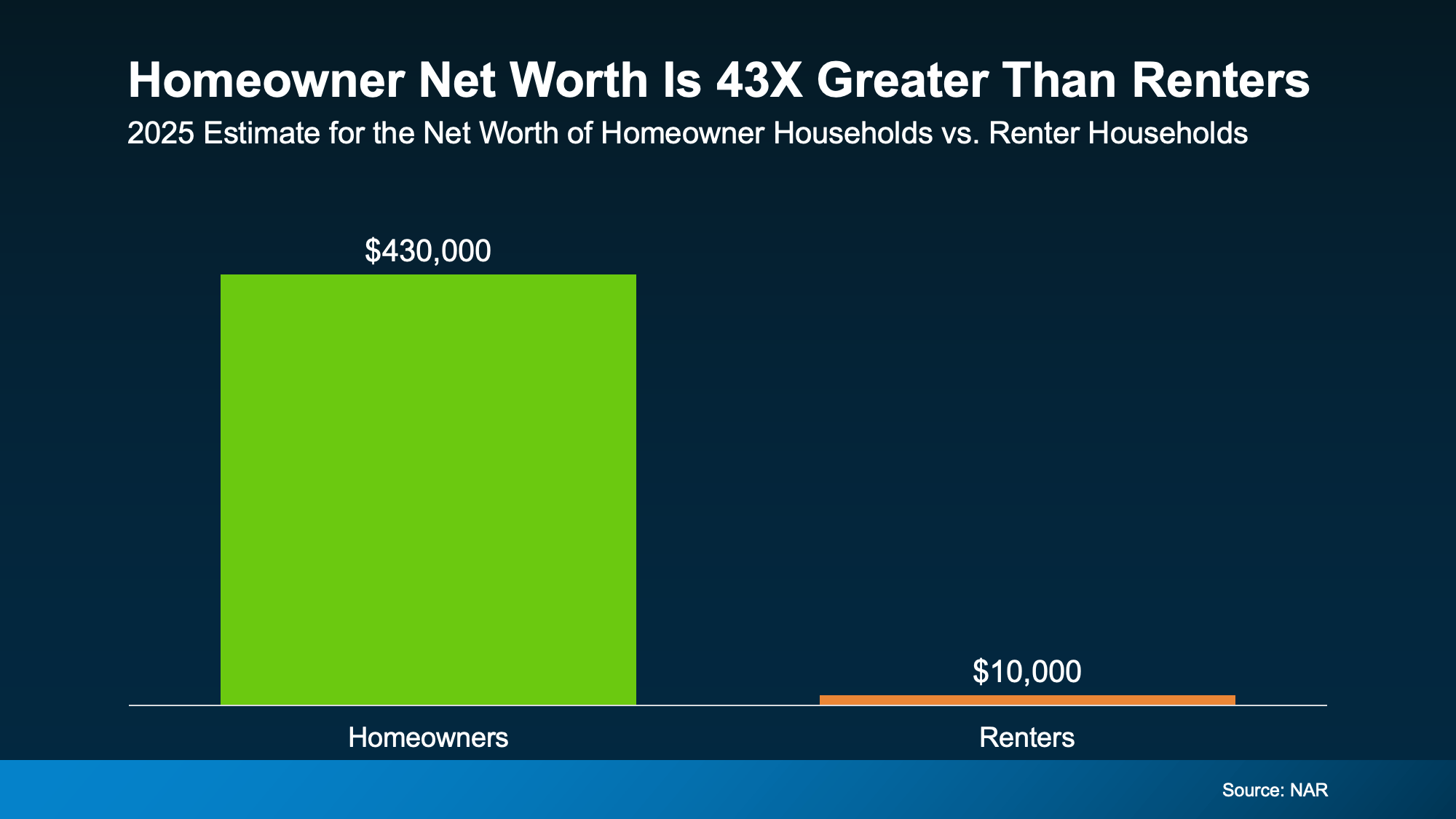

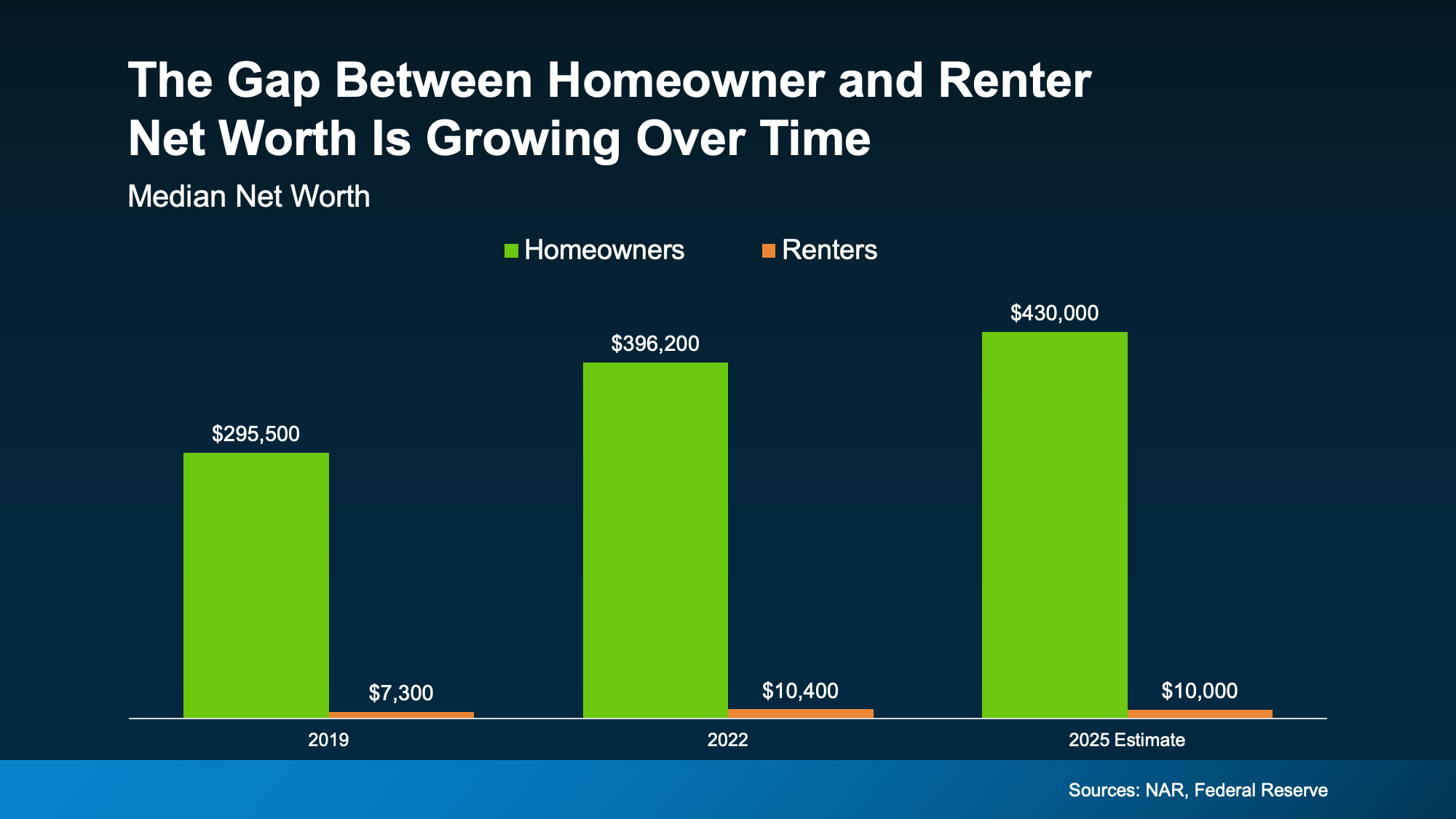

The Wealth Gap Between Owners and Renters Is Striking

This is the number that stops most people cold. According to NAR, the average homeowner’s net worth is roughly 43 times greater than the average renter’s. Homeowners average around $430,000 in net worth. Renters average around $10,000.

That gap is not primarily explained by income differences or smarter financial decisions in other areas. It is explained by one thing: homeowners build equity over time and renters do not. And that gap has been widening, not shrinking. Even in years when home price growth moderated, homeowners continued pulling ahead because their equity kept compounding while renters continued paying without accumulating.

How Equity Actually Builds

Every mortgage payment you make reduces what you owe and increases what you own. At the same time, as home values rise over time (which historically they do, as we covered in Are Home Prices Going To Fall?), the gap between what your home is worth and what you owe widens further. That compounding effect is what makes homeownership such a consistent wealth-building vehicle over time.

It is essentially a forced savings account you can live in. The “cost” of owning, your monthly mortgage payment, is simultaneously building an asset. The cost of renting builds nothing for you.

The Monthly Payment Comparison Is Only Part of the Picture

Buyers often compare a mortgage payment to a rent payment and conclude renting is cheaper. Sometimes that is true in the short term. But that comparison leaves out equity accumulation, appreciation, tax advantages, and the long-term trajectory of each path. A mortgage payment that feels high today is also fixed, while rents tend to increase every year. A renter paying $1,800 today may be paying $2,200 in three years. A homeowner with a fixed-rate mortgage is still paying the same principal and interest they locked in at closing.

For buyers wondering whether the current rate environment changes this math, our post What Rising Inflation Means for Your Move and The Truth About Home Affordability Today both address how today’s rates fit into the longer-term picture.

When Renting Is the Right Call

Buying is not the right move for everyone right now. If you are planning to move within two years, if your finances are not yet in the right place, or if you are in an active period of life transition, renting may absolutely be the more sensible path. The point is not that everyone should buy immediately. The point is to make the decision with full information rather than defaulting to renting because it feels safer without running the actual long-term numbers.

First-Time Buyers: Your Path to Ownership May Be Closer Than You Think

For buyers who want to make the move from renting to owning, the options available right now may surprise you. From VA benefits covered in What Most Veterans Don’t Know About Their VA Home Loan Benefit, to creative approaches like Could Co-Buying Be the Answer for Some First-Time Buyers, to making the most of a tax refund in Getting a Tax Refund? Here’s How It Can Help You Buy a Home, the path to ownership has more on-ramps than most renters realize.

What This Means Right Here in South Jersey

In Collingswood, Oaklyn, Haddon Township, and the surrounding communities, rental prices have been rising steadily while home prices have remained relatively stable. That combination means the gap between renting and owning in our specific market has narrowed meaningfully. For many renters in South Jersey right now, ownership is financially closer than it has been in years.

The question is not whether you should eventually own. The question is what it would take to make it happen on your timeline. That answer starts with a specific, honest conversation about your numbers.

Reach out to the MH Global team. Let’s figure out what the path from renting to owning actually looks like for you right now.